WANT TO BUY OR SELL A PROPERTY?

Frequently Asked Questions About 4% Listings

Frequently Asked Questions About Hiring Me As Your Loan Officer, Realtor® or Both

Frequently Asked Questions About Mortgages

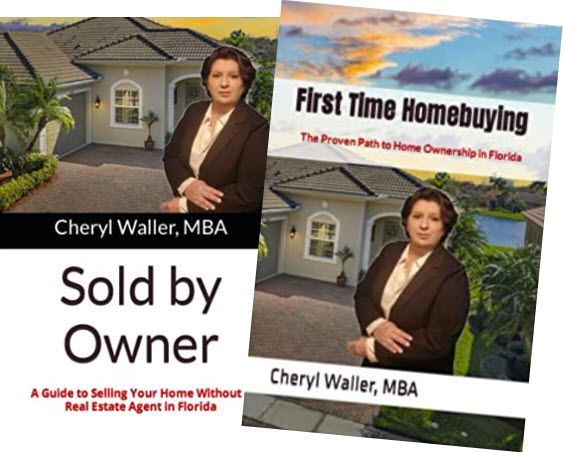

Thinking of Buying or Selling Without a Real Estate Agent?

For Residents of Indian River County, Florida ONLY

Choose Your FREE Paperback Book with FREE Shipping

List Your Property for 4% and

Save

Thousands!

Serving Vero Beach & Indian River County, Florida

Includes FREE CMA and Mortgage Home Valuation (using both real estate & mortgage tools)

Listen to

Cheryl

on 99.7 Jack FM

Looking to Buy? Get up to $35,000 Toward Your New Home

List Your Home for 4% . Save Thousands on Commission!

Call or Text 772-222-6590

Company Lic# CQ1032076

Agent Lic# SL3516742

Serving Vero Beach

& Indian River County, Florida

CHERYL WALLER, MBA

VERO BEACH REAL ESTATE AGENT

Lic# SL3516742

CONTACT

Ocean Capital Real Estate Services Group

Melbourne:

1900 S. Harbor City Blvd Suite 328

Melbourne, FL 32901

Corporate Headquarters:

120 S Olive Ave Suite 311

West Palm Beach, FL 33401

Office: 800-895-7174 Ext. 87

Cell: 772-222-6590

Fax: 800-771-0985

VERO BEACH REAL ESTATE AGENT Cheryl Waller, MBA is a licensed Real Estate Agent #SL3516742 with Ocean Capital Real Estate Services Group #CQ1032076. Cheryl Waller, MBA, is a Member of the National Association of Realtors®, Florida Realtors®, and Broward, Palm Beaches, & St. Lucie Realtors®.

Listing information on this website is provided by third-party brokers through an MLS feed service, is not verified for authenticity or accuracy, and is not guaranteed. Buyers must verify property information. Community and neighborhood information may be incorrect or may have changed since posted on this website. No information presented on this website is guaranteed to be accurate. All information is provided for convenience only.